Quarterly Outlook

Macro outlook: Trump 2.0: Can the US have its cake and eat it, too?

John J. Hardy

Global Head of Macro Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Macro events: UK Retail Sales (Jul), US University of Michigan Prelim (Aug)

Earnings: Flowers Foods, CINT, OneConnec

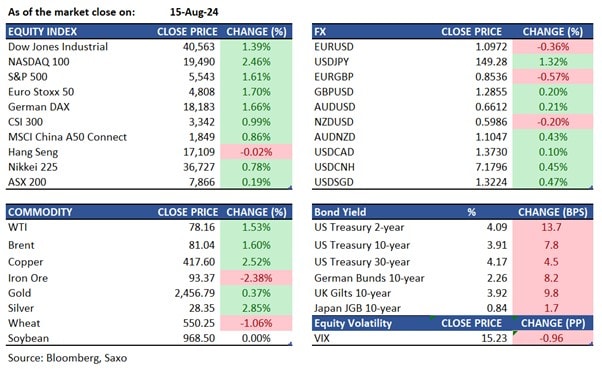

Equities: US stocks surged on Thursday as Wall Street responded positively to signs of strength in the US consumer and labor markets, easing recession worries. The S&P 500 and the Nasdaq extended their winning streak to six days, gaining 1.6% and 2.4%, respectively, while the Dow Jones rose by 555 points. The rally was driven by strong economic data, including retail sales that increased by 1% in July, far exceeding the expected 0.3% rise. Additionally, weekly jobless claims fell to their lowest level since early July, further boosting sentiment. All sectors closed in the green, with consumer discretionary leading, followed by tech and materials. On the earnings front, Cisco's optimistic revenue forecast pushed its shares up 6.8%, while Walmart advanced 6.6% after beating earnings and revenue expectations. In extended hours, Applied materials fell 3% despite beating earnings estimates and forecasting this quarter’s sales in line with its guidance.

Fixed income: Treasury futures dropped sharply, and the yield curve aggressively flattened after retail sales exceeded estimates and jobless claims came in below expectations. This bear-flattening trend persisted into a quiet afternoon, though yields later eased from their lowest levels. US yields were cheaper by up to 14 basis points on the front end, while 30-year yields rose by around 5 basis points. The 10-year yield ended the day at 3.92%, peaking at 3.95%. Futures volumes were 4% above the 20-day average, with the 5-year note contract seeing 10% higher activity. Following the data, Fed swaps reduced the likelihood of a half-point rate cut at the September meeting, with 29 basis points of easing priced in, down from 32. For December, 92 basis points of easing were priced in, down from 102. Money-market fund assets hit a record high as $28.4 billion flowed in, reaching $6.22 trillion. China's US Treasuries holdings rose to the highest level since the start of the year, while Japanese investors sold the most Treasuries since September 2022.

Commodities: Oil prices fell as the market weighed strong US economic data and the potential threat of an attack by Iran or its proxies on Israel against weak demand in China. West Texas Intermediate dropped below $78 a barrel after a 1.5% rise on Thursday, while Brent crude closed just above $81. Robust US retail sales and employment figures mitigated concerns about sluggish investment and industrial activity in China. Global benchmark Brent is set for a second weekly gain, rebounding from a seven-month low. The market remains on alert for developments in the Middle East, as Israel entered talks about pausing the conflict in Gaza. Gold prices fluctuated as traders processed US retail spending data, considering the outlook for the Federal Reserve’s expected interest-rate cuts next month. Copper prices rose for the second day, balancing weak Chinese economic data against labor disruptions at the world’s largest mine. London prices increased by roughly 2%, building on Wednesday’s gains. China’s economic downturn extended into the third quarter, while efforts to resolve a labor dispute at BHP Group’s Escondida mine in Chile stalled.

FX: The US dollar faced two opposing forces, with rising Treasury yields pushing it higher but offset by reduced recession concerns supporting a risk-on sentiment and pushing the US dollar lower. The Japanese yen, however, suffered on both accounts and has retraced all its gains since recession concerns first picked up with the July US jobs report on August 2. Activity currencies, however, saw a sharp rebound after the initial US retail sales-driven decline. UK’s pound as well as Australian dollar were eventually higher against the US dollar, while others like the euro stayed weak.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Please read our disclaimers:

- Notification on Non-Independent Investment Research (https://www.home.saxo/legal/niird/notification)

- Full disclaimer (https://www.home.saxo/en-gb/legal/disclaimer/saxo-disclaimer)