Quarterly Outlook

Fixed Income Outlook: Bonds Hit Reset. A New Equilibrium Emerges

Althea Spinozzi

Head of Fixed Income Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Macro events: Japan’s ruling LDP party leadership election, China Industrial Profits (Aug), German Unemployment (Sep), EZ Consumer Confidence Final (Sep), US PCE (Aug), Uni. of Michigan Final (Sep)

Earnings: No major earnings

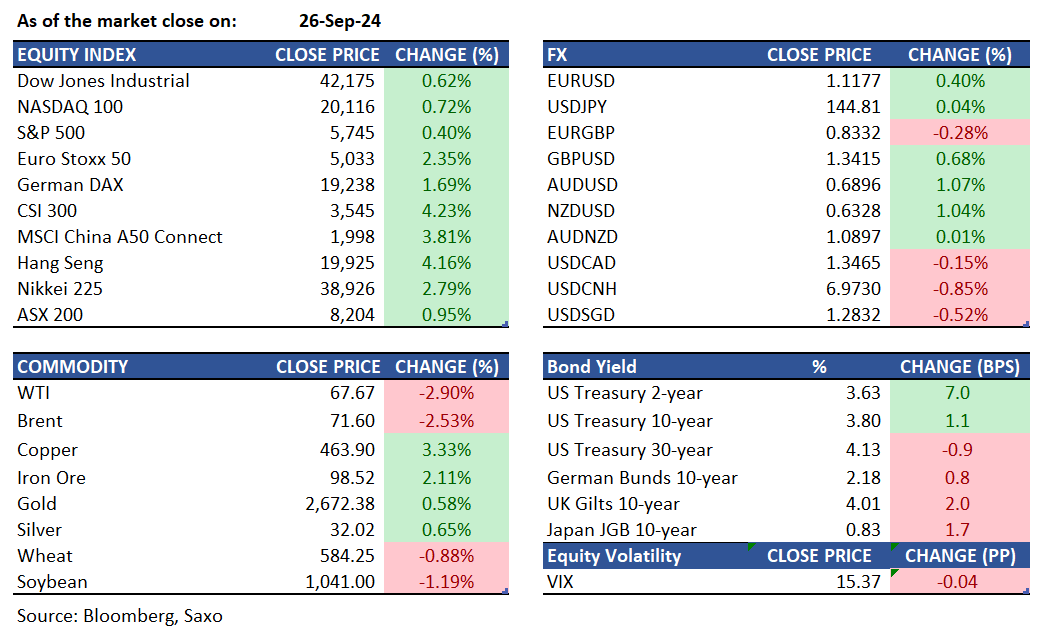

Equities: On Thursday, the S&P 500 rose 0.4% to reach a new record high, while the Nasdaq gained 0.6%, and the Dow Jones added 260 points. Investor sentiment was buoyed by strong corporate earnings and positive economic data. Micron Technology led the charge, surging 14.7% after an optimistic earnings forecast, which sparked gains across the semiconductor sector. Applied Materials climbed 6.2%, and Lam Research advanced 5.4%. The rally was further supported by encouraging economic reports, including weekly jobless claims falling to a four-month low, indicating a strong labor market. Additionally, second-quarter GDP growth was confirmed at a robust 3%. China stimulus continues to boost sentiment with the Golden Dragon Index up 10.8% and KraneShares CSI China Internet ETF up 11.5%. Hang Seng Index was also up 4.1% in Asia session yesterday and Hang Seng futures were up a further 2.7% overnight. For more on how China stimulus measures can impact markets, read this article.

Fixed income: The Treasuries curve flattened significantly as long-end yields declined and 2-year yields rose by 6 basis points from Wednesday's close, reflecting a reduced Fed rate cut premium in overnight swaps. Losses intensified ahead of the 7-year note auction, which concluded strongly, trading 0.7 basis points through the when-issued yield. Treasury yields were up to 6 basis points higher at the front end, with the 2s10s spread flattening by 6 basis points on the day. The US 10-year yield hovered around 3.785%, nearly unchanged, as the curve pivoted around this sector. The 2s10s spread saw its most significant flattening in over a month, dropping to as low as 16.2 basis points late in the session. Additionally, the amount of reserves in the banking system, a key factor for the Federal Reserve's balance sheet reduction, fell to its lowest level since April 2023.

Commodities: Gold rose by 0.57% to settle at $2,672, supported by China's stimulus commentary. It remains a strong uncorrelated hedge for equity portfolios, bolstered by central bank buying, though it may face profit-taking as momentum appears stretched. Silver extended its strong momentum to reach $32.5 per ounce in late September, its highest in 12 years, driven by expectations of incoming rate cuts by the Federal Reserve. WTI crude futures declined overnight and failed to rally despite positive China stimulus news and favorable economic data. The November contract fell by 2.9% to $67.67, while Brent dropped by 2.53% to $71.60. A Financial Times report suggested that Saudi Arabia might abandon its $100 per barrel target and increase production to regain market share, likely driving the price decline despite attempts by bulls to counter the story. Copper futures rose by 3.33% to $463.90, hovering close to over two-month highs on reports that top consumer China will be rolling out more stimulus measures to support the economy.

FX: The US dollar pared much of its gains as risk-on returned due to the optimism on China’s stimulus measures. The Chinese yuan was back below the 7-handle against the US dollar while the Australian dollar and kiwi dollar outperformed as commodity currencies remain in the spotlight amid optimism that China’s demand could return. High-beat British pound also rose higher. The Swiss franc also defied any pressures given the SNB rate cut was well-expected and there was also an odd chance of a 50bps cut. The only G10 currency that ended lower against the US dollar was the Japanese yen, but losses have been constrained ahead of the LDP elections due today and US PCE out later. The euro and Canadian dollar also underperformed.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Head of Commodity Strategy

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Please read our disclaimers:

- Notification on Non-Independent Investment Research (https://www.home.saxo/legal/niird/notification)

- Full disclaimer (https://www.home.saxo/en-gb/legal/disclaimer/saxo-disclaimer)