Quarterly Outlook

Fixed Income Outlook: Bonds Hit Reset. A New Equilibrium Emerges

Althea Spinozzi

Head of Fixed Income Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Macro events: Japan/Australia/Eurozone/UK/US Flash PMIs, BoC Policy Decision, German GfK

Earnings: AT&T, Ford, IBM, Thermo Fisher Scientific, Waste Management

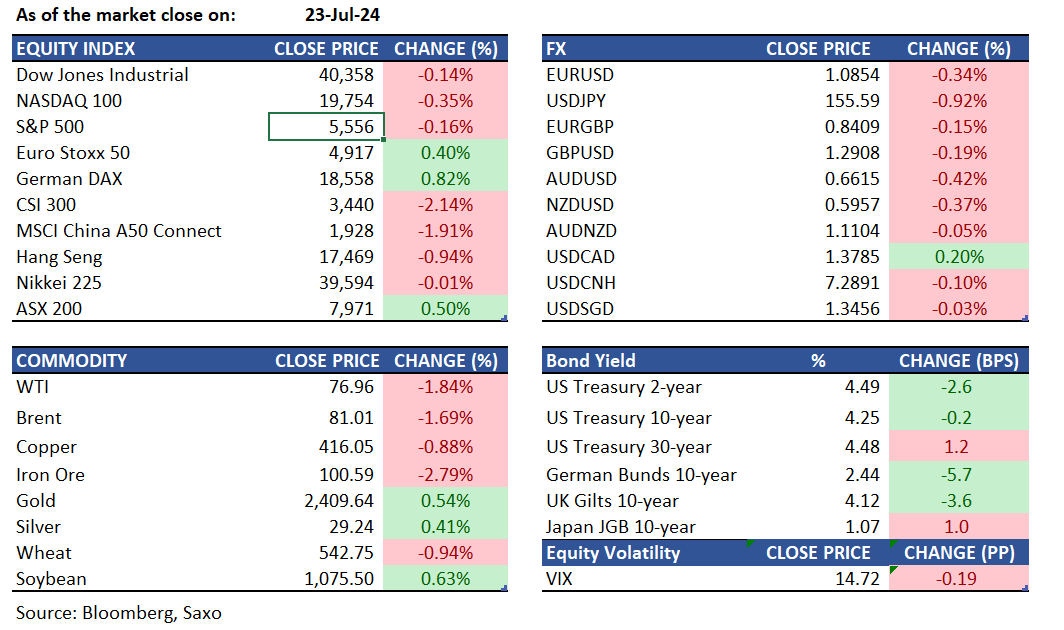

Equities: U.S. stocks ended the session flat with mixed earnings from key names. SAP shares jumped 7.2% on strong results, boosting software stocks, while SPOT rallied 12% on its results and subscriber numbers. GM posted solid results, but shares reversed lower after reaching 52-week highs. Tesla reported profits that missed estimates for the fourth straight quarter, resulting in a 7.8% fall post-market. Alphabet's earnings topped estimates, but the stock fell 2% after hours. Economic data continues to be soft, with existing home sales for June falling -5.4% M/M and a larger negative reading from the Richmond Fed for July.

Fixed income: Treasuries ended Tuesday with mixed results, as the yield curve steepened following robust demand for the $69 billion 2-year note auction. Investors secured a combined 91% of the auction, the highest since 2003, while primary dealers received a record low of 9%. The 2s10s curve inversion eased to about -24 basis points, nearing the least-inverted levels of the year. The Treasury is set to auction $30 billion in two-year floating-rate notes and $70 billion in five-year debt on Wednesday. Meanwhile, Japan’s Ministry of Finance will auction ¥700 billion in March 2064 bonds via a tap sale. Futures of Japan’s 10-year notes fell 10 ticks to 142.8, while the benchmark 10-year yield remained steady at 1.06%.

Commodities: Brent crude fell 1.7% to $81, and WTI dropped 1.8% to $76.96, hitting their lowest levels in over a month due to renewed Israel-Hamas ceasefire talks and demand concerns. Despite a 3-week decline in US crude inventories, summer gasoline demand remains weak. Investors await API's oil inventory estimates and official US data. The upcoming OPEC+ meeting on August 1 is not expected to change output policies. Gold price continued to decline yesterday but has stabilized in early trading this morning, closing back above $2400. Silver prices dropped below $29, approaching their lowest levels since mid-May due to a weakened demand outlook in China, the leading consumer, which affected investor sentiment. Copper declined to around $4.15, marking their lowest point since early April amid worries over demand from China, the largest consumer.

FX: The US dollar was higher on Tuesday across most major currencies, but fell against the Japanese yen. The yen has seen broad strength as US yields continue to fall in the run up to the Fed meeting next week where Chair Powell could acknowledge the progress on bringing inflation back towards the target and potentially open the door to a September rate cut. Meanwhile, expectation for the Bank of Japan to hike rates again next week is also underpinning and pushing Japanese yields higher. Activity currencies such as the Norwegian krone, New Zealand dollar and the Australian dollar, meanwhile, continue to weaken with commodity prices on a decline and equities also seemingly losing momentum. Canadian dollar will be on watch today with Bank of Canada meeting on tap, and recent decline in the Loonie could mean that further weakness would need a rate cut and dovish language along with it.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Head of Commodity Strategy

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Please read our disclaimers:

- Notification on Non-Independent Investment Research (https://www.home.saxo/legal/niird/notification)

- Full disclaimer (https://www.home.saxo/en-gb/legal/disclaimer/saxo-disclaimer)