Quarterly Outlook

Fixed Income Outlook: Bonds Hit Reset. A New Equilibrium Emerges

Althea Spinozzi

Head of Fixed Income Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Macro events: UK Unemployment, Canada Inflation, Fed Daly Speech

Earnings: Interactive Brokers, Johnson&Johnson, UnitedHealth Group, Goldman Sachs, Bank of America, Citigroup, Charles Schwab

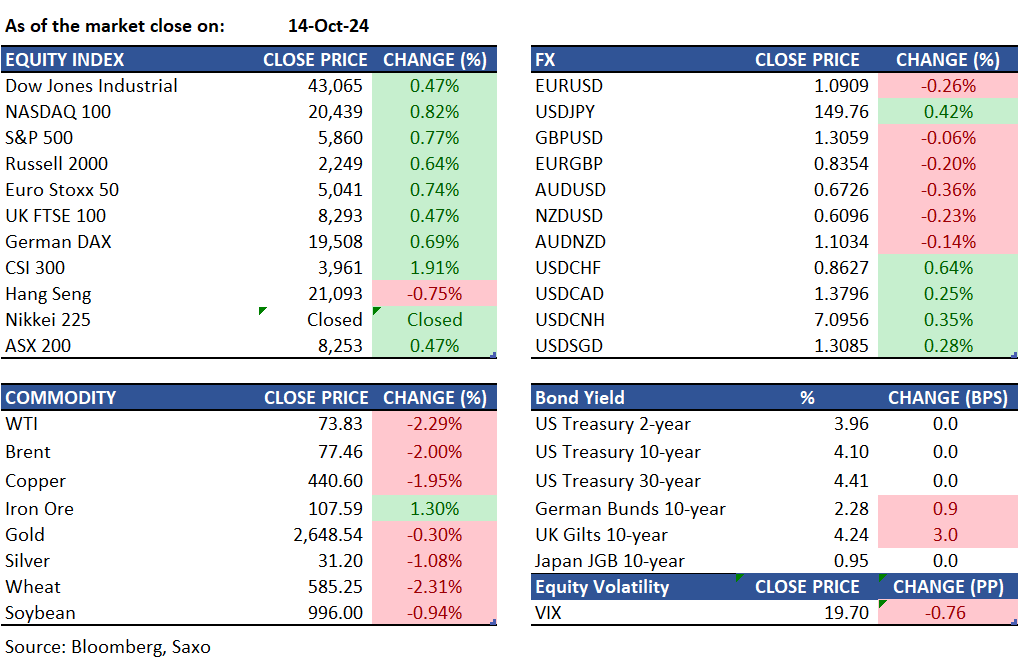

Equities: On Monday, the S&P 500 and Dow Jones reached new record highs, gaining 0.77% and 0.47% respectively while the Nasdaq 100 climbed 0.8%, driven by strong performances in tech stocks. Nvidia closed at all time highs of $138.07 after gaining 2.4% while the chip sector continues to outperform. Arm holdings led the pack with a 6.8% rally, with Qualcomm gaining 4.7%, Applied Materials up 4.3% and ASML climbing 3.7%. This week, the earnings season intensifies with major companies like UnitedHealth, J&J, Bank of America, Goldman Sachs, and Netflix set to report their results.

Fixed income: Cash Treasury yields are anticipated to reopen slightly lower by a few basis points after the US holiday. Futures declined in the morning, driven by losses in European rates. UK bonds underperformed as investors positioned for a £2.25 billion 30-year UK bond auction scheduled for Tuesday. An early large block sale in bund futures also contributed to the downward pressure. US 10-year yields are expected to reopen at approximately 4.12%, a few basis points lower than Friday's close. 10-year note futures fell by about 12 ticks but ended above the session lows reached during the US morning session. UK 10- and 30-year yields rose by up to 5 basis points, reaching 4.26% and 4.80%, respectively. Meanwhile, Italy’s yield premium over Germany decreased to its lowest level since March 21.

Commodities: Oil prices fell sharply, with WTI crude dropping 2.29% to $73.83 and Brent crude oil futures declining 2.5% to around $77. This decline followed OPEC's reduction of its global oil demand growth forecast for 2024 and 2025, and reports that Israel will not target Iranian crude infrastructure. OPEC now expects world oil demand to rise by 1.93 million bpd in 2024, down from the previous forecast of 2.03 million bpd. China's crude imports for the first nine months of the year decreased nearly 3% from last year to 10.99 million bpd. Additionally, China's recent stimulus plans did not boost investor confidence, and markets are closely watching for potential Israeli attacks on Iranian oil infrastructure. Gold prices also dropped to near $2,648 after rising for five consecutive weeks.

FX: The dollar strengthened against all G10 currencies in US holiday-thinned trading as traders assessed China’s fiscal stimulus and Fed comments. The yen weakened toward the key 150 per dollar level. The Bloomberg Dollar Spot Index rose 0.3%, with the Swiss franc and Norway’s krone leading losses. USDJPY rose 0.6% to a session high of 149.98; surpassing 150 would be the first time since August 1. The yen has been the worst-performing G10 currency year-to-date, down 5.6% against the dollar. Hedge funds bought yen for the second consecutive week, according to CFTC data. USDCAD advanced for the ninth straight session to 1.3797, matching a July streak that was the longest since 2017. The Swiss franc was among the session’s worst performers, with USDCHF rising 0.7% to 0.8630.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Head of Commodity Strategy

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Please read our disclaimers:

- Notification on Non-Independent Investment Research (https://www.home.saxo/legal/niird/notification)

- Full disclaimer (https://www.home.saxo/en-gb/legal/disclaimer/saxo-disclaimer)