Quarterly Outlook

Macro outlook: Trump 2.0: Can the US have its cake and eat it, too?

John J. Hardy

Global Head of Trader Strategy

Key points:

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

The data will be used to help shape expectations for the December FOMC meeting, where the vast majority of analysts expect a 25bps rate cut, while money market pricing is assigning 70% probability of a rate cut. Governor Waller has said that he favours a 25bps rate cut in December, and while some other members have hinted at caution at the pace of easing – that is more a 2025 story. Mary Daly speaks after the NFP release and her comments could be key to shape up December Fed expectations, but a 300k+ headline print may be needed to dissuade the Fed from cutting rates this month. For a trader’s preview of the NFP, read this article.

Equities:

FX:

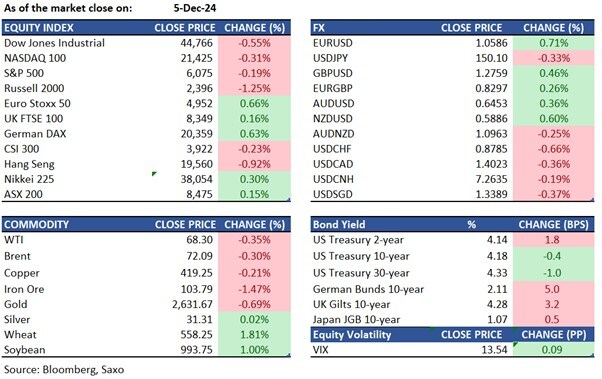

Commodities: WTI crude stayed near $68 per barrel as OPEC+ maintained Q1 2025 production levels, planning gradual increases until September 2026. U.S. data showed a large stockpile drop but record production. Gold fell below $2,630 per ounce due to rising Treasury yields. Silver held above $31 per ounce on Fed rate cut bets. Copper traded around $4.14 per pound, amid speculation of Beijing stimulus measures.

Fixed income:

For a global look at markets – go to Inspiration.

Quarterly Outlook

Global Head of Trader Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Trader Strategy

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist