Quarterly Outlook

Macro outlook: Trump 2.0: Can the US have its cake and eat it, too?

John J. Hardy

Global Head of Macro Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Macro events: FOMC Announcement (preview here), BoJ Announcement and Outlook Report (preview here), China NBS PMI (Jul), Australia CPI (Q2/Jun), German Retail Sales (Jun), French CPI Prelim. (Jul), EZ Flash HICP (Jul), Italian CPI Prelim. (Jul), US ADP (Jul), Pending Home Sales (Jul), Chicago PMI (Jul)

Earnings: Boeing, Mastercard, Meta, Arm, Qualcomm, Lam Research

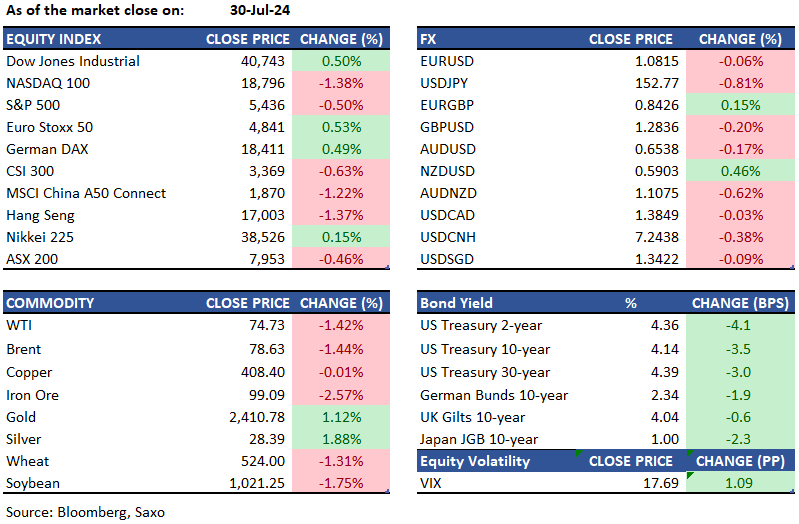

Equities: US stocks erased early gains as declines in heavyweight chip companies pressured tech-exposed equity indices, while markets assessed recent data and geared up for the Federal Reserve’s policy decision tomorrow. The Nasdaq 100 closed 1.3% lower, reaching its lowest level in nearly two months, while the S&P 500 fell 0.5%. Nvidia dropped 7%, triggering widespread selling pressure on other semiconductor giants and extending the sector's period of weakness as investors question the sustainability of the AI rally, shifting their focus to more traditional sectors of the US economy. Microsoft fell as much as 3% post-market after reporting a miss on cloud revenue, while AMD rallied 7.6% after reporting earnings that surpassed expectations and issued a strong Q3 forecast. On the other hand, Apple, Alphabet, and Meta experienced muted activity ahead of their reports later in the week. Merck sank 9.8%, and Procter & Gamble plunged 4.8% following their respective results. Still, the Dow gained 205 points, extending its outperformance over tech-heavy counterparts, supported by banks and insurers.

Fixed income: Treasuries closed Tuesday with lower yields and a slightly steeper curve, reaching session lows in the US afternoon amid a haven rally following Israel's strike in Lebanon targeting a Hezbollah commander. Five- and 10-year yields dropped to their lowest levels since March. Earlier, the market faced a brief setback when June JOLTS job openings and July consumer confidence exceeded economist expectations. Yields decreased by 3 to 5 basis points. Balances at the Federal Reserve’s overnight reverse repurchase agreement facility fell to their lowest level in over six weeks, as repo rates remained above the program's offering yield. Japanese bond futures tumbled overnight after media reports suggested that the nation's central bank might consider raising the policy interest rate. About 30% of BOJ watchers anticipate a rate hike, while over 90% acknowledge the risk of such a move. The benchmark yield dropped 3 basis points to 0.995%.

Commodities: Gold increased by 1.12%, closing at $2,410, while silver up 1.88% to $28.39 on Tuesday, close to 12-week lows, as investors anticipated upcoming monetary policy decisions from major central banks. WTI crude dropped by 1.42% to $74.73 per barrel, marking a 9% decline in July and reaching its lowest level since early June. Brent crude futures also fell 1.44% to $78.63 per barrel due to easing geopolitical risks and concerns over Chinese demand. Copper futures continued their decline, reaching $4 per pound, the lowest in four months, amid growing demand concerns from China.

FX: The Japanese yen rallied sharply overnight amid reports from Japanese media about a potential rate from the Bank of Japan at the announcement today. The Swiss franc also gained this morning in Asia amid escalating Mideast tensions fueling safe-haven flows. Meanwhile, the US dollar also remained supported despite the 1% gain in Japanese yen. The resilience of the British pound is coming under scrutiny as the Bank of England decision draws closer and an August rate cut remains a coin toss. The Australian dollar has also been on a backfoot ahead of the quarterly inflation report out today, where a hot print can continue to fuel speculation about a potential rate hike from the Reserve Bank of Australia.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Please read our disclaimers:

- Notification on Non-Independent Investment Research (https://www.home.saxo/legal/niird/notification)

- Full disclaimer (https://www.home.saxo/en-gb/legal/disclaimer/saxo-disclaimer)