Quarterly Outlook

Macro outlook: Trump 2.0: Can the US have its cake and eat it, too?

John J. Hardy

Global Head of Trader Strategy

Key points:

------------------------------------------------------------------

The Saxo Quick Take is a short, distilled opinion on financial markets with references to key news and events.

Disclaimer: Past performance does not indicate future performance.

In the news:

Macro:

Earnings: Procter & Gamble, American Express, Schlumberger, Comerica, Fifth Third Bank

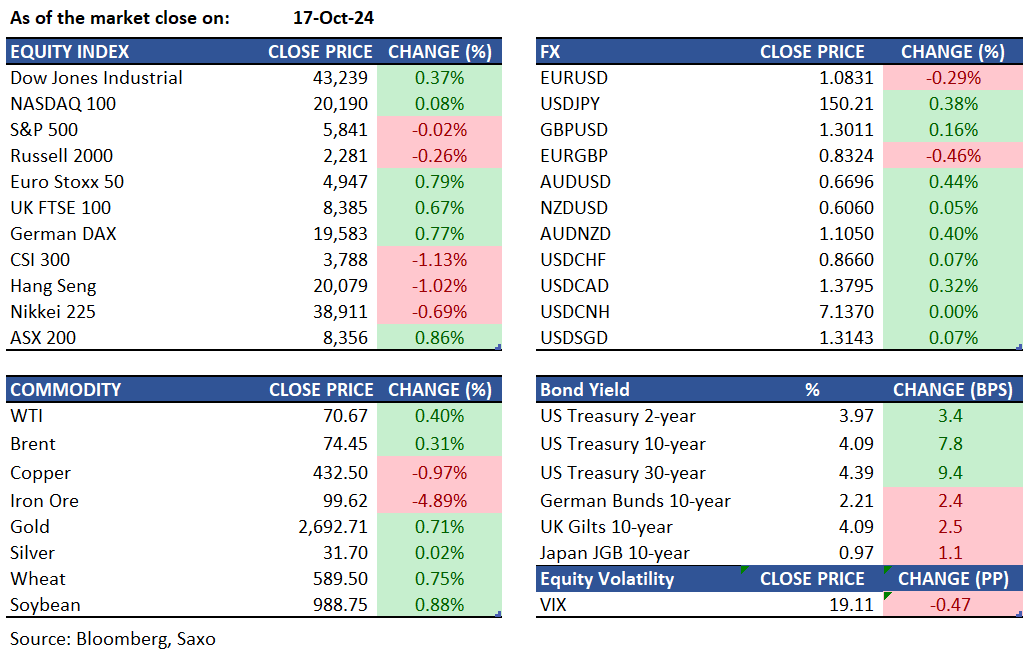

Equities: US stocks traded mostly higher Thursday afternoon, with semiconductor shares driving the gains after strong corporate and economic news. The S&P 500 ended the session flat after briefly touching a new record, the Dow Jones was up over 100 points after hitting all time highs of 43,272, and the Nasdaq 100 rose 0.3%. Nvidia surged 3% to a new record high after its key supplier, Taiwan Semiconductor (TSMC), posted robust Q3 earnings that showed a 54% yoy growth and also raised its revenue outlook. TSMC’s shares spiked 11%, lifting other chipmakers higher like Broadcom (2.6%) and Micron (2.57%). US data continues to outperform with retail sales data for September showing a 0.4% rise vs 0.3% est, which further bolstered sentiment. Additionally, jobless claims came in lower than forecast, reinforcing the view that consumer spending remains resilient. Netflix reported earnings after the close which showed that they beat top and bottom line estimates and they added more than 5 million subscribers in Q3, exceeding expectations of about 4 million.

Fixed income: Treasuries fell after stronger-than-expected September retail sales and upward revisions to August figures, along with a drop in weekly initial jobless claims. Initial losses led by the front end flattened the yield curve, but it ended steeper due to long-end underperformance. Long-end yields rose about 9 basis points, while front-end and belly yields increased by 3 to 7 basis points. The 10-year yield climbed over 7 basis points to 4.09%, just 1 basis point below the day's high. Movement was driven by economic data releases and supported by euro-zone bonds, where investors anticipated larger ECB rate cuts following comments from President Lagarde. German front-end yields declined by about 2 basis points.

Commodities: Gold prices rose by 0.71% to $2,692, reaching new all-time highs earlier in the session. This increase occurred despite gains in yields and the US Dollar. The rise is attributed to uncertainty ahead of the US elections and ongoing tensions in the Middle East, which continue to position gold as a safe-haven asset. Technical indicators also favor buyers. Although economic data was stable this morning, investors anticipate future easing by the Federal Reserve. Meanwhile, November WTI crude futures climbed by 0.40% to $70.67, and Brent crude increased by 0.31% to $74.45. These gains were supported by better-than-expected US economic data and a weekly inventory draw, contrary to the expected build. The improved economic outlook has led investors to lean towards a soft landing rather than a recession for now. Iron ore futures fell below $100 as a Chinese government briefing failed to introduce aggressive property sector policies. Officials announced expanding a 'white list' of real estate projects and increasing bank lending to 4 trillion yuan, but markets were disappointed by the reliance on existing measures.

FX: A Bloomberg index of the dollar rose after strong US consumer spending and labor data led traders to scale back their expectations of interest-rate cuts from the Federal Reserve. The euro declined as European Central Bank officials highlighted growth risks while lowering borrowing costs. EURUSD dropped to a session low of 1.0811 as the ECB cut interest rates for the third time this year, bringing the key deposit rate to 3.25%. The yen weakened past the critical 150 level after US data strengthened the dollar, with USDJPY reaching a session high of 150.30, its highest since August 1, leading G-10 losses. USDCAD reversed Wednesday’s decline, climbing 0.3% to 1.3795. The Australian dollar outperformed after Australia's unemployment rate remained steady, prompting traders to delay their expectations of RBA rate cuts next year.

For all macro, earnings, and dividend events check Saxo’s calendar.

For a global look at markets – go to Inspiration.

Quarterly Outlook

Global Head of Trader Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Trader Strategy

Quarterly Outlook

Head of Fixed Income Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Please read our disclaimers:

- Notification on Non-Independent Investment Research (https://www.home.saxo/legal/niird/notification)

- Full disclaimer (https://www.home.saxo/en-gb/legal/disclaimer/saxo-disclaimer)