口座開設は無料。オンラインで簡単にお申し込みいただけます。

最短3分で入力完了!

チーフ・インベストメント・ストラテジスト

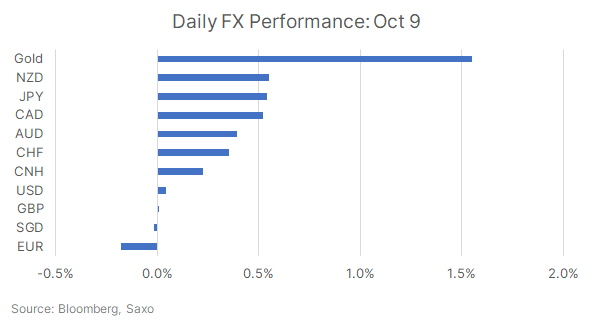

サマリー: 金曜に雇用統計が好結果となり、月曜には週末の痛ましい事件を受けて安全志向が強まったにもかかわらず、米ドル指数(DXY)の上昇トレンドは難航し始めている。FRBメンバーもタカ派色を薄めており、焦点は今週のインフレ・データに移っている。一方、イスラエル・シェケルの下落は中央銀行の介入によって食い止められた。

※本レポート内日本語は、ご参考情報として原文(英語)を機械翻訳したものです。

先週、ドル指数は11週連続で上昇していたが、金曜の雇用統計の結果を受け、下落に転じた。週明けのドル円相場は、週末の中東情勢を受けた安全志向から買いが先行した。しかし、その月曜の買い戻しも続かず、DXY指数は現在106のサポートにしがみつくのに苦労している。果たして、米ドル上昇トレンドは終焉に近づいているのだろうか。

米ドル上昇トレンドを反転させるには、米国経済が悪化する明確な兆候が必要であることを強調してきた。しかし、現時点では強い雇用統計と地政学的緊張のさらなる高まりしかない。このことがドル高をもう一段下支えしているはずだが、値動きから読み取れるメッセージは「疲弊」というものだ。FRBはタカ派も含めて、市場がFRBに代わって利上げを行うため、再利上げの可能性を否定し始めた。昨日、ジェファーソンとローガン(通常はタカ派)は、ともにFOMCの投票者だが、利回りの動きと金融引き締めへの影響は、FRBがそれほど多くのことをする必要がないことを意味するかもしれないと認めた。この解説では、11月の利上げが織り込まれている確率はわずか12%(以前は30%)、最初の全面利下げは2024年6月と見られるなど、金融市場ではハト派的なリプライシングが見られた。

一方、米ドルの上昇余地が弱まる可能性があるとしても、FRBが長期金利上昇を緩和するほど経済が弱まるまでは、明確な下降トレンドは回避される可能性がある。サクソの債券ストラテジスト、アルテア・スピノッツィもまた、イールドカーブの前部に張り付いてディフェンシブな姿勢を保つ理由を強調している。彼女は、今週の10年債と30年債の入札が利回りの低下をサポートすることが可能であると考えている。米国の財政赤字が依然として懸念されるなか、豊富な国債供給とイスラエル情勢がさらにエスカレートするリスクが引き続きドルを支える可能性がある。また、利回りの高さが経済に打撃を与え始めているため、リスク資産も依然として圧力下に置かれる可能性が高く、ドル・エクスポージャーはヘッジとしての役割を引き続き担うだろう。

マーケット分析:米ドルの上昇傾向は弱まりつつあるが、ドルが上昇に転じる可能性は高い:上昇トレンドラインと21DMAの105.8を下回ると、104.39が露呈する可能性がある。

雇用と地政学に続き、今週発表される米インフレ指数にも注目が集まるだろう。ここ数週間のイールドカーブの急上昇は、市場が目先の景気後退リスクよりも、長期的にインフレが高水準で推移することを依然として懸念していることを示唆している。一方、最近の原油価格とガソリン価格の上昇が、ヘッドラインインフレ率を押し上げている。8月に前年同月比3.7%まで急上昇したヘッドラインインフレ率だが、原油価格が月内にやや落ち着きを見せたことから、前年同月比3.6%までやや冷え込むと現在市場は予想している。

コアCPIもまた、家賃やシェルター・インフレの下落により低下する可能性が高いが、自動車保険や医療サービスなど、その他のサービス・カテゴリーは引き続き堅調に推移する可能性がある。消費者物価指数(コアCPI)は8月の前年同月比4.3%から9月は同4.1%に低下するとコンセンサスは予想している。これは、全体的なディスインフレ傾向は維持される可能性があることを意味するが、地政学的情勢が新たなリスクに直面しており、コモディティ価格をめぐる不確実性を考えると、軟調なインフレ指標からあまり安心するのは時期尚早かもしれない。FRBがこの不安定な環境下で利上げに踏み切る可能性は低く、強い上方修正のサプライズがない限り、11月の金融政策決定会合では利上げが見送られる可能性が高い。しかし、経済データが弱まらない限り、FRBは長期金利上昇のメッセージを押し続けるだろう。一方、11月1日のFOMC決定に向けては、米GDP速報値(10月26日予定)やPCE(10月27日予定)など、その他の重要データが注目される。

コアCPIが予想を上回れば、長期金利上昇のシナリオがさらに強まり、米ドルがさらに上昇し、日本円や豪ドル、NZドルなどのリスク選好通貨が重くなる可能性がある。しかし、予想を下回れば、市場がすでに織り込んでいること、すなわちFRBの一時休止の延長が再確認されることになる。

イスラエル・シェケルは、週末のハマスの攻撃を受けて圧力を受けている。攻撃以前は、イスラエル政府による司法改革と弱体化の計画が物議を醸し、通貨の重荷となっていた。しかしながら、週末の出来事により、USDILSは2016年以来の高値をつけた。

このため、USDILSは昨日の高値3.9622から3.92に向かって反落した。イスラエルの中央銀行は、その豊富な外貨準備高を考慮し、引き続きボラティリティを平滑化する可能性がある。

Summary: The dollar index (DXY) uptrend is starting to get challenged despite the blowout headline jobs report on Friday and the safety bid on Monday following the tragic events over the weekend. Fed members are also turning less hawkish and focus shifts to inflation data this week which could continue to fuel the higher-for-longer narrative. Meanwhile, the slide in Israeli shekel was stalled by central bank intervention.

The dollar index closed lower last week after steady gains in the last 11 weeks, despite Friday’s blowout NFP report on the headline. The index started the week with a bid coming from a rush to safety after the unfortunate developments in the Middle East region over the weekend. However, that Monday bid was also not sustained and the DXY index is now struggling to hold on to its 106 support. Does that mean that the dollar uptrend may be coming close to an end?

We have highlighted before that clear signs of deterioration in the US economy will be needed to reverse the dollar uptrend. But all we have got for now is the strong NFP report and a further uptick in geopolitical tensions. While that should have underpinned another leg of strength in the dollar, the message coming across from the price action is one of exhaustion. Fed speaker, including some of the hawkish ones, have started to talk down the case for another rate hike as markets do the job for the Fed. Jefferson and Logan (usually a hawk) – both FOMC voters – yesterday acknowledged that the move in yields and its impact on tightening financial conditions may mean that the Fed may not have to do as much. The commentary saw dovish repricing in money markets with just a 12% probability of a hike being priced in for November (from 30% earlier) with the first full rate cut seen in June 2024.

Meanwhile, even as USD upswing room may be starting to weaken, a clear downtrend could evade until economy weakens enough to let the Fed loosen its higher-for-longer message. Saxo’s fixed income strategist Althea Spinozzi has also continued to highlight reasons to stay defensive and stick to the front-part of the yield curve. She thinks that the 10-year and 30-year Treasury auctions this week could provide support to declining yields. With US fiscal deficit still a concern, abundant Treasury supplies and risks of further escalation in the Israel situation could continue to provide support for the dollar. Risk assets are also likely to remain under pressure as high yields start to hurt the economy, and dollar exposure continues to serve as a hedge.

After jobs and geopolitics, focus may also be turning to US inflation numbers due this week. Bear steepening of the yield curve in the recent weeks suggests that markets are still more concerned about inflation remaining high in the long run than the risk of a recession in a near term. Meanwhile, the rise in oil and gasoline prices recently is pushing headline inflation higher. After the surge to 3.7% YoY in August, consensus now expects some cooling in headline inflation to 3.6% YoY as oil prices steadied somewhat in the month.

Core CPI is also likely to be pulled lower due to the decline in rents and shelter inflation, but some of the other services categories such as car insurance and medical services could remain sticky. Consensus expects core CPI to cool to 4.1% YoY in September from 4.3% in August. While that means overall disinflation trends could remain intact, taking too much comfort from a soft inflation print may be premature given the uncertainty around commodity prices with the geopolitical landscape facing fresh risks. Fed is unlikely to hike rates in this volatile environment, and barring any strong upside surprises, rates may likely stay on hold at the November meeting. But as long as economic data does not weaken, Fed will keep pressing on its higher-for-longer message. Meanwhile, other key data such as advance US GDP (due on 26 October) and PCE (due on October 27) will be on watch ahead of the FOMC decision on 1 November.

That leads us to believe that a higher-than-expected core CPI print could give further legs to the higher-for-longer narrative, boosting USD further and weighing on JPY as well as risk sensitive currencies like AUD and NZD. However, a softer-than-expected print will just reaffirm what the markets have already priced in – an extended Fed pause.

The Israeli shekel has come under pressure after the weekend attack from Hamas. Prior to the attacks as well, the controversial plans by the Israeli government to reform and weaken the judiciary have weighed on the currency, but weekend events brough USDILS to its highest levels since 2016.

The Bank of Israel (BoI) announced yesterday that it is prepared to sell up to $30 billion from its $203 billion FX reserves to support the shekel, and this could also be extended by $15 billion through swap mechanisms. This helped USDILS to drop back towards 3.92 from highs of 3.9622 yesterday. Israel’s central bank could continue to smoothen the volatility given its large FX reserves.